Chapter 5 11

th

edition

1

MERCHANDISING OPERATIONS AND THE MULTI-STEP

INCOME STATEMENT

LO 1: Describe merchandising operations and inventory systems.

• Primary source of revenue for merchandisers like Walmart that buy and sell goods is referred to as

sales revenue.

• Cost of goods sold is the total cost of merchandise sold during the period.

o It is an EXPENSE that is directly related to the revenue recognized from the sale of goods.

Ex: Company C, a retailer, bought chairs from a wholesaler for $15 each. Company C then sold the

chairs to their customers for $20 each.

• The $20 represents Company C’s sales revenue for each chair.

• The $15 that Company C spent on each chair represents Company C’s cost of goods sold and

is recognized when each chair is sold to customers.

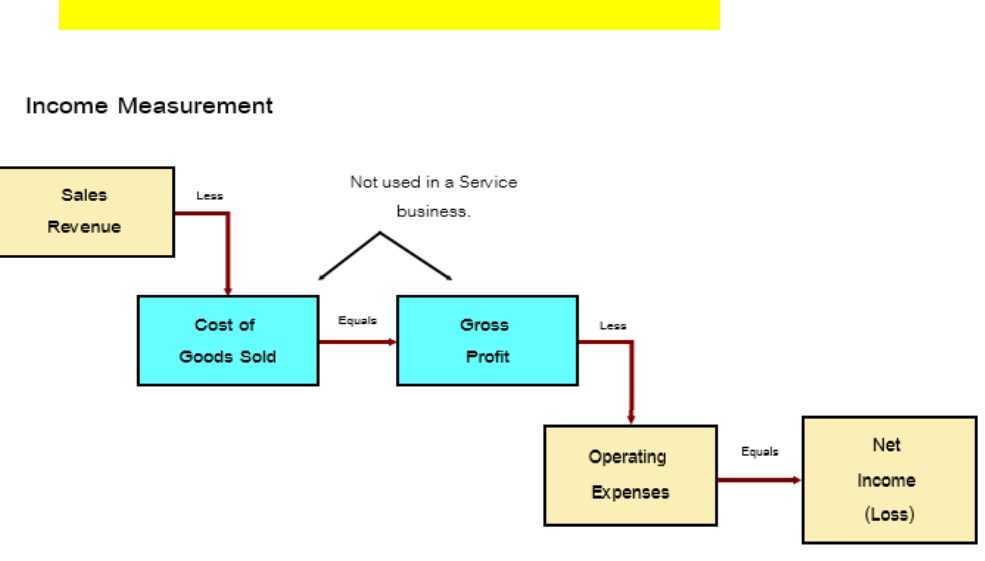

***Key Formula: Sales Revenue – Cost of Goods Sold = Gross Profit

Chapter 5 11

th

edition

2

FLOW OF COSTS

• Companies use either a perpetual inventory system or a periodic inventory system to account for

inventory.

1. Perpetual: CONTINUOUSLY updates accounting records for merchandising transactions –

SPECIFICALLY reduction of inventory and increasing cost of goods sold.

• Advantages of perpetual inventory system.

1. Traditionally used for merchandise with high unit values.

2. Shows the quantity and cost of the inventory that should be on hand at any time.

3. Provides better control over inventories than a periodic system.

2. Periodic: updates the accounting records for merchandise transactions at the END OF A PERIOD.

• Cost of goods sold determined by count at the end of the accounting period.

***Key Formula… Cost of Goods Sold = Beginning Inventory + Net Purchases – Ending Inventory

Beginning Inventory

200,000$

Add: Purchases, net

900,000$

Goods available for sale 1,100,000$

Less: Ending Inventory 400,000$

Cost of Goods Sold 700,000$

Chapter 5 11

th

edition

3

LO 2: Record purchases under a perpetual inventory system.

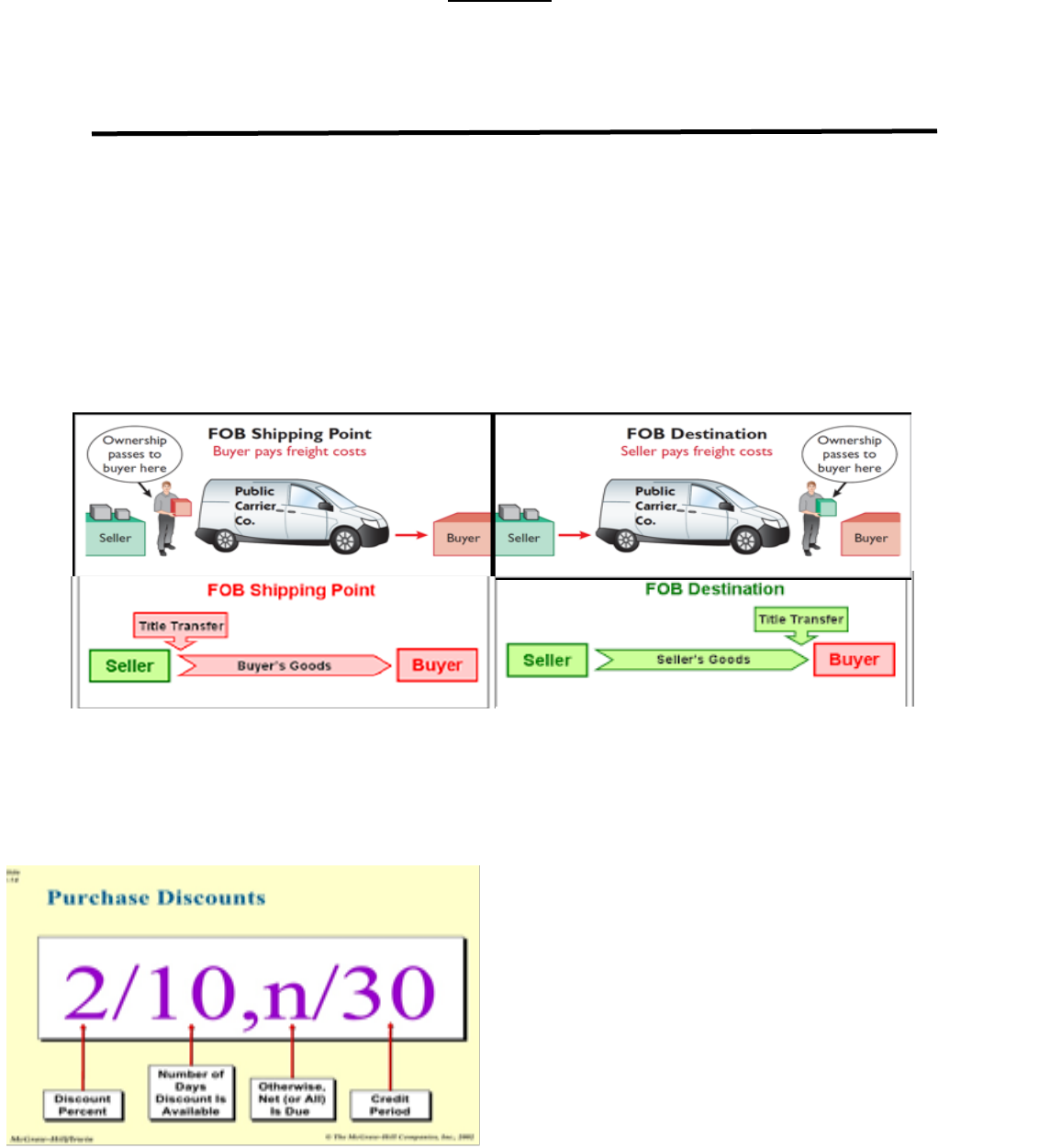

FREIGHT COSTS

Shipping Terms Ownership Transfers when goods passed to Freight cost paid by

PURCHASE DISCOUNTS

• Buyer receives a cash discount for prompt payment.

• Saves the buyer money and helps the seller collect money faster.

What does this mean?

*The buyer can deduct 2% of the invoice amount if

payment is made within 10 days of the invoice

date, otherwise full payment is due within a

30-day credit period.

*Simply…The buyer gets a 2% discount if they pay

within 10 days, otherwise the full amount is due in

30 days.

1. FOB (Free on Board)

Shipping Point: GOODS

ARE BUYERS AS SOON AS

CARRIER GETS THEM.

2. FOB (Free on Board)

Destination: GOODS ARE

SELLERS UNTIL THEY REACH

BUYER.

1. CARRIER

2. BUYER

1. BUYER

Inventory xxx

Cash xxx

2. SELLER

Freight-Out xxx

Cash xxx

Del

Chapter 5 11

th

edition

4

PURCHASE DISCOUNTS (Cont.)

PURCHASE RETURNS AND ALLOWANCES

• Purchase Returns: Return goods for credit if the sale was made on credit, or for a cash refund if the

purchase was for cash.

• Purchase Allowances: May choose to keep the merchandise if the seller will grant a reduction of

the purchase price.

1% discount if paid within first 10 days of next month.

Net amount due within the first 10 days of the next month.

DEBIT CREDIT

Inventory xxx

Accounts Payable xxx

Inventory xxx

Cash xxx

Inventory xxx

Cash xxx

Accounts Payable xxx

Inventory (For purchase discount) xxx

Cash xxx

Accounts Payable xxx

Cash xxx

Cash or Accounts Payable xxx

Inventory xxx

2. Purchase inventory for CASH.

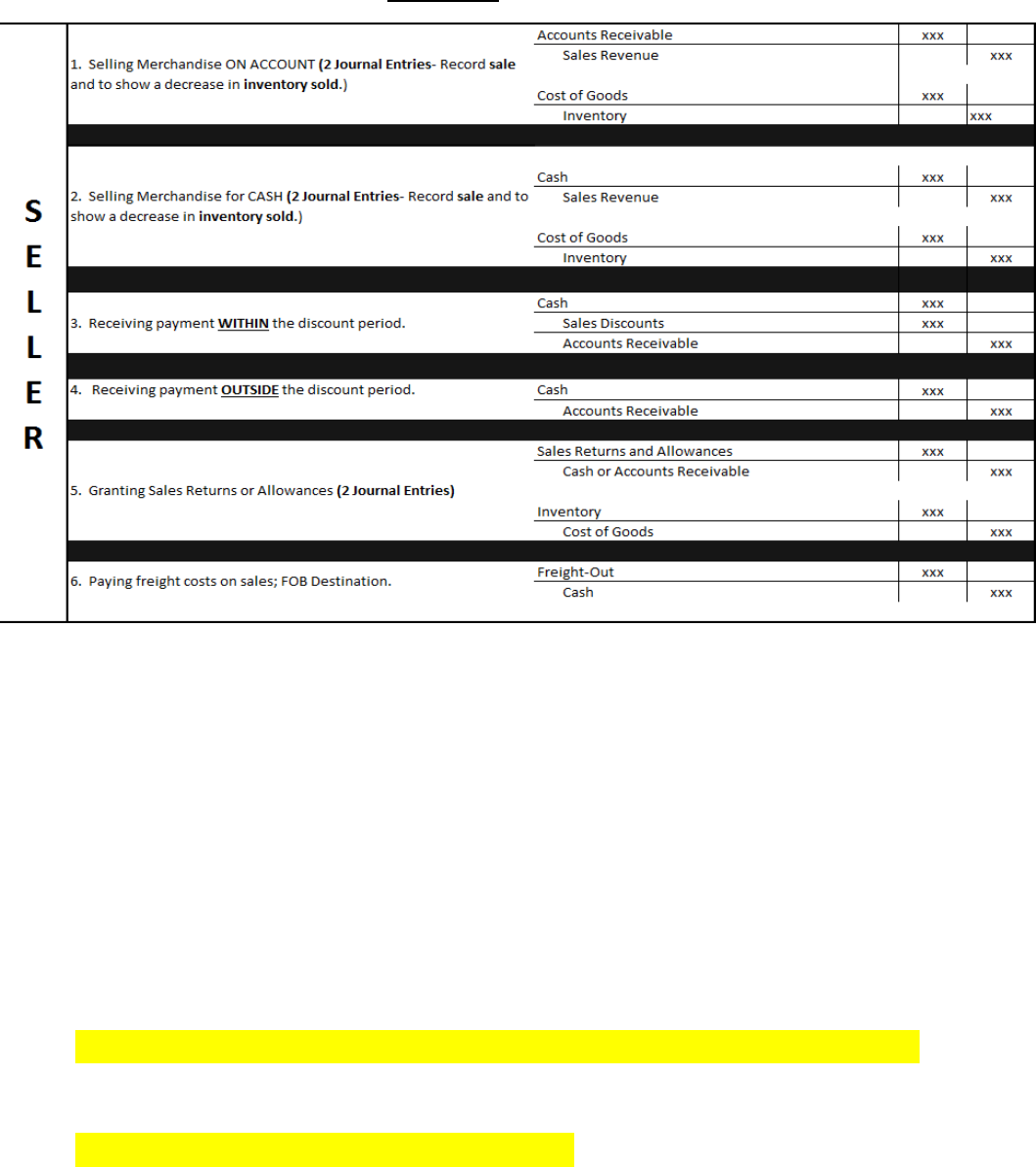

Summary of Purchasing Journal Entries- Perpetual

B

U

Y

E

R

1. Purchase inventory ON ACCOUNT.

3. Paying freight costs on purchases (FOB Shipping Point)

4. Paying WITHIN discount period.

5. Paying OUTSIDE discount period.

6. Recording Purchase Returns and Allowances.

Chapter 5 11

th

edition

5

Example Journal Entries

Jay Company bought inventory from Z Company on January 1 for $10,000 under the credit terms 3/15,

n/60. On January 10, Jay Company returned goods costing $1,000 to Z Company. Jay Company paid Z

Company for the remaining goods on Jan. 12.

What are the journal entries that need to be recorded in January for Jay Company?

Date

Debit

Credit

Inventory

Jan. 1

10,000

Accounts Payable- Z Company

10,000

Accounts Payable- Z Company

Jan. 10

1,000

Inventory

1,000

Accounts Payable- Z Company (10,000 – 1,000)

Jan. 12

9,000

Inventory (9,000 × 3% = $270)

270

Cash

8,730

Chapter 5 11

th

edition

6

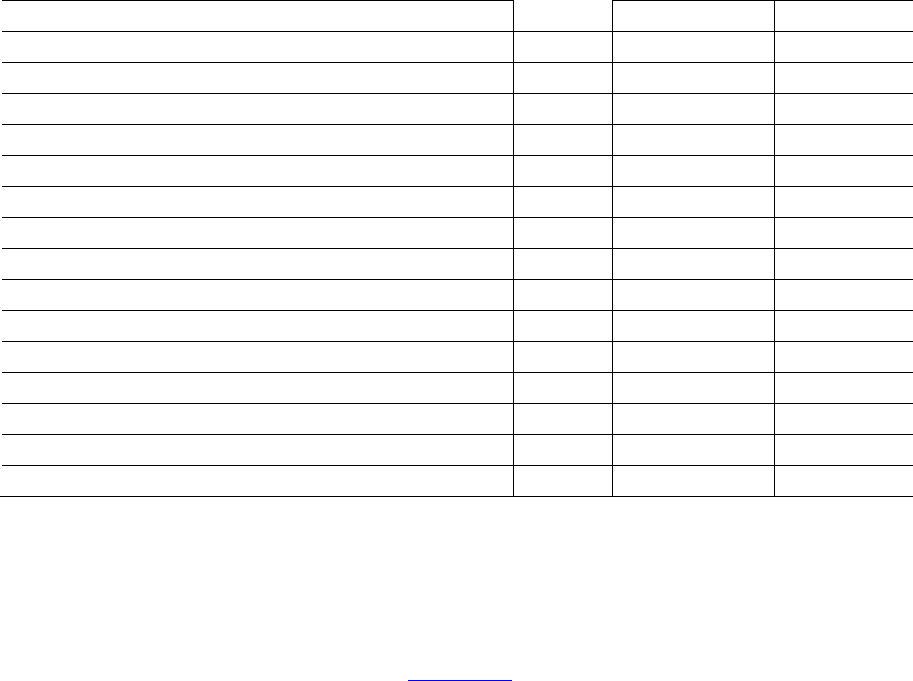

LO 3: Record sales under a perpetual inventory system.

SALES RETURNS AND ALLOWANCES

• Used when the seller either accepts goods back from a purchaser (a return) or grants a reduction in

the purchase price (an allowance) so that the buyer will keep the goods.

• Contra-revenue account on the income statement and has a Debit balance.

SALES DISCOUNTS

• Issued by the seller to obtain their money from the customer faster.

• Contra-revenue account on the income statement and has a Debit balance.

Sales Revenue – Sales Returns and Allowances – Sales Discounts = Net Sales

Net Sales – Cost of Goods Sold = Gross Profit

Chapter 5 11

th

edition

7

Example Journal Entries

• Jay Company sold goods costing $6,000 to X Company for $10,000 on March 1 under the terms

2/10, net 30. On March 5, X Company returned goods to Jay Company with a selling price of $3,000

and a cost of $1,800. On March 10, Jay Company received payment from X Company for the

remainder of the goods.

What are the journal entries that need to be recorded on in March for Jay Company?

Date

Debit

Credit

Accounts Receivable- X Company

Mar. 1

10,000

Sales Revenue

10,000

Cost of Goods Sold

Mar. 1

6,000

Inventory

6,000

Sales Returns and Allowances

Mar. 5

3,000

Accounts Receivable- X Company

3,000

Inventory

Mar. 5

1,800

Cost of Goods Sold

1,800

Cash

Mar. 10

6,860

Sales Discounts (7,000 × 2% = $140)

140

Accounts Receivable- X Company (10,000 -3,000)

7,000

LO 5: Apply the steps in the accounting cycle to a merchandising company.

Each of the required steps described in Chapter 4 for service companies applies to

merchandising companies.

Adjusting Entries

A merchandising company generally has the same types of adjusting entries as a service

company. However, a merchandiser using a perpetual system will require one additional

adjustment to make the records agree with the actual inventory on hand. Here’s why: At the end

of each period, for control purposes, a merchandising company that uses a perpetual system will

take a physical count of its goods on hand.

The company’s unadjusted balance in Inventory usually does not agree with the actual amount of

inventory on hand. The perpetual inventory records may be incorrect due to recording errors,

theft, or waste. Thus, the company needs to adjust the perpetual records to make the recorded

inventory amount agree with the inventory on hand.

Chapter 5 11

th

edition

8

• This adjustment impacts Inventory and Cost of Goods Sold.

For example, suppose that PW Audio Supply, Inc. has an unadjusted balance of $40,500 in

Inventory.

Through a physical count, PW Audio Supply determines that its actual merchandise inventory at

December 31 is $40,000. The company would make an adjusting entry as follows.

Dec. 31

Cost of Goods Sold

500

Inventory ($40,500 – $40,000)

500

(To adjust inventory to physical count)

Closing Entries

A merchandising company, like a service company, closes to Income Summary all accounts that

affect net income. In journalizing, the company credits all temporary accounts with debit

balances, and debits all temporary accounts with credit balances. It also closes both Income

Summary and Dividends to Retained Earnings. (Hint – R.E.D – temporary accounts are

Revenue, Expense, and Dividends)

The following are the closing entries for PW Audio Supply using assumed amounts from its

year-end adjusted trial balance.

• Cost of Goods Sold is an expense account with a normal debit balance,

• Sales Returns and Allowances and Sales Discounts are contra revenue accounts with

normal debit balances

The easiest way to prepare the first two closing entries is to identify the temporary

accounts by their balances and then prepare one entry for the credits and one for the

debits.

Dec.31

Sales Revenue

480,000

Income Summary

480,000

(To close income statement accounts with credit

balances)

31

Income Summary

450,000

Sales Returns and Allowances

12,000

Sales Discounts

8,000

Cost of Goods Sold

316,000

Salaries and Wages Expense

64,000

Freight-Out

7,000

Advertising Expense

16,000

Chapter 5 11

th

edition

9

Utilities Expense

17,000

Depreciation Expense

8,000

Insurance Expense

2,000

(To close income statement accounts with debit

balances)

31

Income Summary

30,000

Retained Earnings

30,000

(To close net income to retained earnings)

31

Retained Earnings

15,000

Dividends

15,000

(To close dividends to retained earnings)

After PW Audio Supply has posted the closing entries, all temporary accounts have zero

balances. Also, Retained Earnings has a balance that is carried over to the next period

LO 5: Prepare a multi-step income statement

SINGLE-STEP INCOME STATEMENT

• Subtract total expenses from total revenues

• Two reasons for using the single-step format:

1. Company does not realize any type of profit or income until total revenues exceed total

expenses.

2. Form is simple and easy to read.

Chapter 5 11

th

edition

10

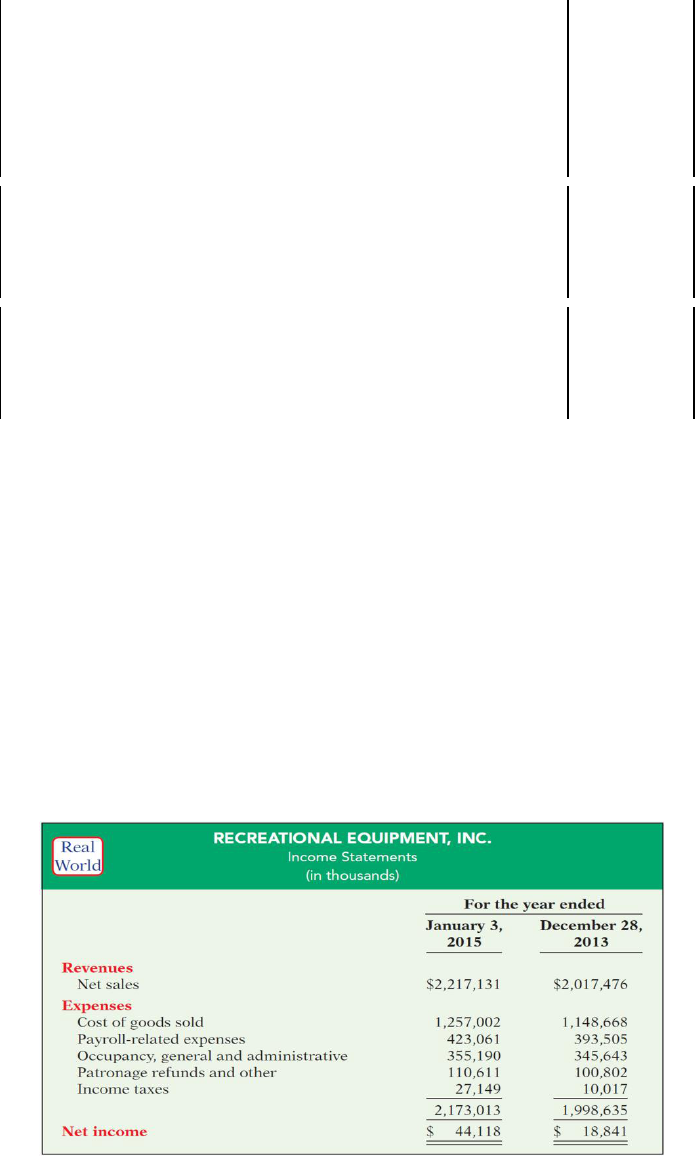

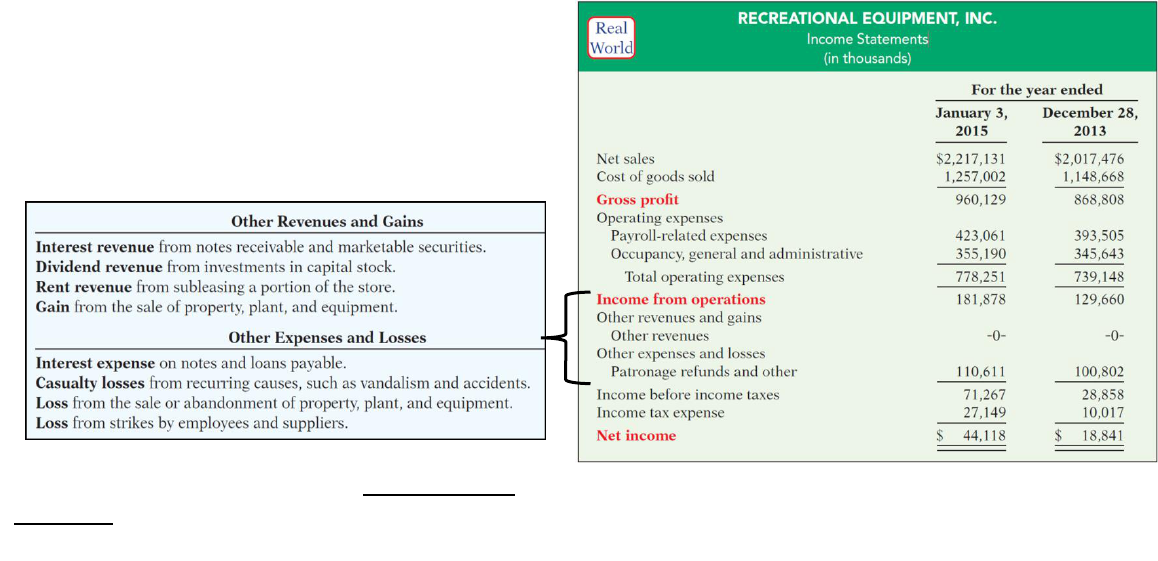

MULTI-STEP INCOME STATEMENT

• Highlights the components of net income.

• Three important line items:

1. Gross profit

2. Income from Operations

3. Net Income

•

***ALL OF THESE ITEMS ARE PART OF NONOPERATING

ACTIVITIES AND ARE ADDED OR DEDUCTED FROM INCOME

FROM OPERATIONS TO GET INCOME BEFORE TAXES.

{kind=link}